Index: please click on the link for the index please?

The Central Bank Plan to Monopolize Global Finance

Werner points out that while central banks are promoting CBDCs as digital currency, we’ve had digital currency for decades, so there’s nothing new about the digital aspect of this currency. Cash — paper banknotes and coins — are but a small part — about 3% in most countries — of the total money supply. The rest is digital.

Today, central banks are the only ones authorized to issue banknotes, but regular banks create 97% of the money through lending. They’re not allowed to issue paper notes. Instead, they issue deposit entries into your bank account, which is digital. So, Werner notes, you could say we’ve been using bank digital currency (BDC) for decades.

The difference between BDCs and CBDCs is the centralized aspect. So, what’s happening now is that central banks, which are the regulators of banks, are stepping in to directly compete with the banks they’re regulating. Werner likens it to the umpire joining the game. That obviously makes it an unfair game.

“It is a big danger,” Werner tells Cummins.2“And you can see where this is going. If we allow central bank digital currencies, sooner or later they will drive out the private sector competition. They will drive out the banks.

And, of course, we also have this other problem … that whenever we get a banking crisis and a financial crisis, the regulators get more power because each time they argue, ‘Oh that now happened, it’s different from before and that’s because we still don’t have enough power. We need to have more powers’ …

This is a regulatory moral hazard. If the regulator gets rewarded for failure … you can be sure that we’ll have more crises, because they’ll be given more powers. Now they want to introduce CBDCs, and of course, the best time from their viewpoint is … another banking crisis, so that people want to move their money out of banks …

That’s the easiest way to introduce this, which means we have a massive incentive now for regulators, for central planners, to create another huge financial crisis so that they can then take over.

Of course, then that’s the end of it, because the banking system is not going to recover from this. Now, do we really want this, where essentially the number of banks goes down so much that there’s really only one bank left?

In their 23 years or so of existence, the ECB has killed around 5,000 banks in Europe already, and it wasn’t the big guys … Thousands of banks are gone in America too, and, of course, JP Morgan and the rest are hoovering them up so they’re just becoming big fat mega banks …

It seems the ECB is set up to be the … only bank they want left in Europe, and that’s going to happen if we allow CBDCs. So, we really have to step up now and say, ‘We don’t need this; we already have digital currencies, thank you very much.’”

The longer America remains a lone superpower, the greater the Federal Reserve’s reach over global finance.

After a pandemic and multiple financial crises, we’ve finally entered a lengthy period of rising interest rates. But while most are aware of the ominous outcomes this could create, those who understand how the Fed actually controls interest rates will gain an edge in predicting the future.

Because of recent events ushering in exceptional circumstances, current textbooks describing how the Fed influences interest rates have become obsolete. Until recently, Federal Reserve officials could simply raise and lower interest rates by decreasing and increasing the level of bank reserves in the financial system. Bank reserves are “interbank” money, which can only be used by entities with reserve accounts inside the Federal Reserve System. JPMorgan, for instance, can pay Goldman Sachs for prime New York real estate using its reserves, while the average citizen must use bank deposits or “Federal Reserve Notes,” a fancy term for physical cash.

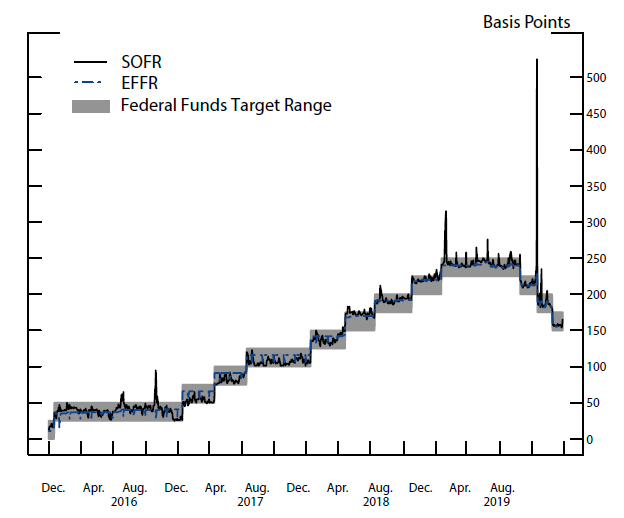

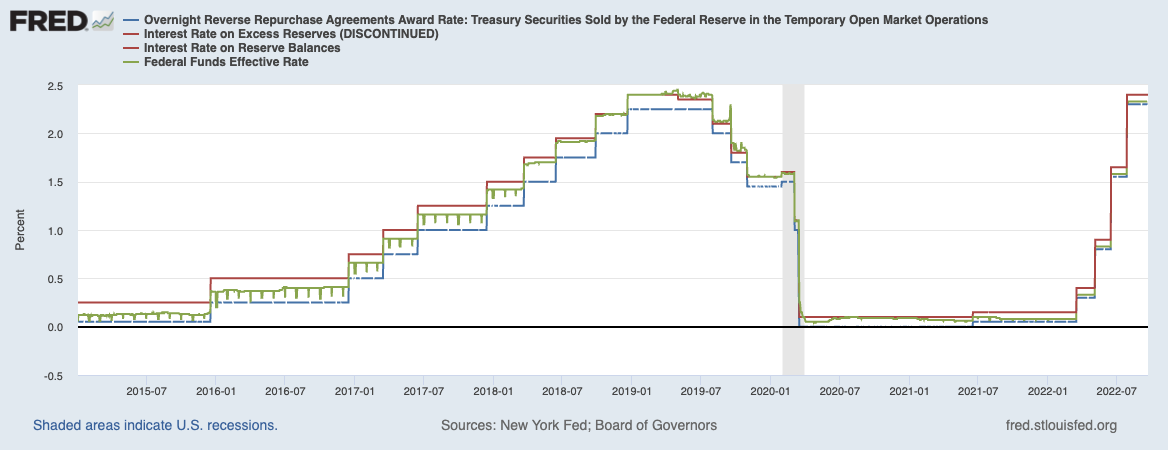

Before the Great Financial Crisis (GFC), the Federal Reserve had enough power to push interest rates toward its target, commonly known as the Federal Funds rate or EFFR — the price at which banks lend reserves to one another. The U.S central bank did so by adding and removing a specific amount of reserves to and from its interbank system. By lowering the supply of bank reserves, the Fed forced financial institutions to bid up the price of Federal Funds, resulting in higher interest rates throughout money markets. Conversely, by increasing the supply of bank reserves, the Fed influenced interest rates lower. The following graphic from the St. Louis Fed website illustrates these forces at work.

Everything ran smoothly. The Fed set a target range in which interest rates could fluctuate and made the necessary adjustments to keep rates within set boundaries. Conveying and implementing its latest monetary policy stance was a cakewalk.

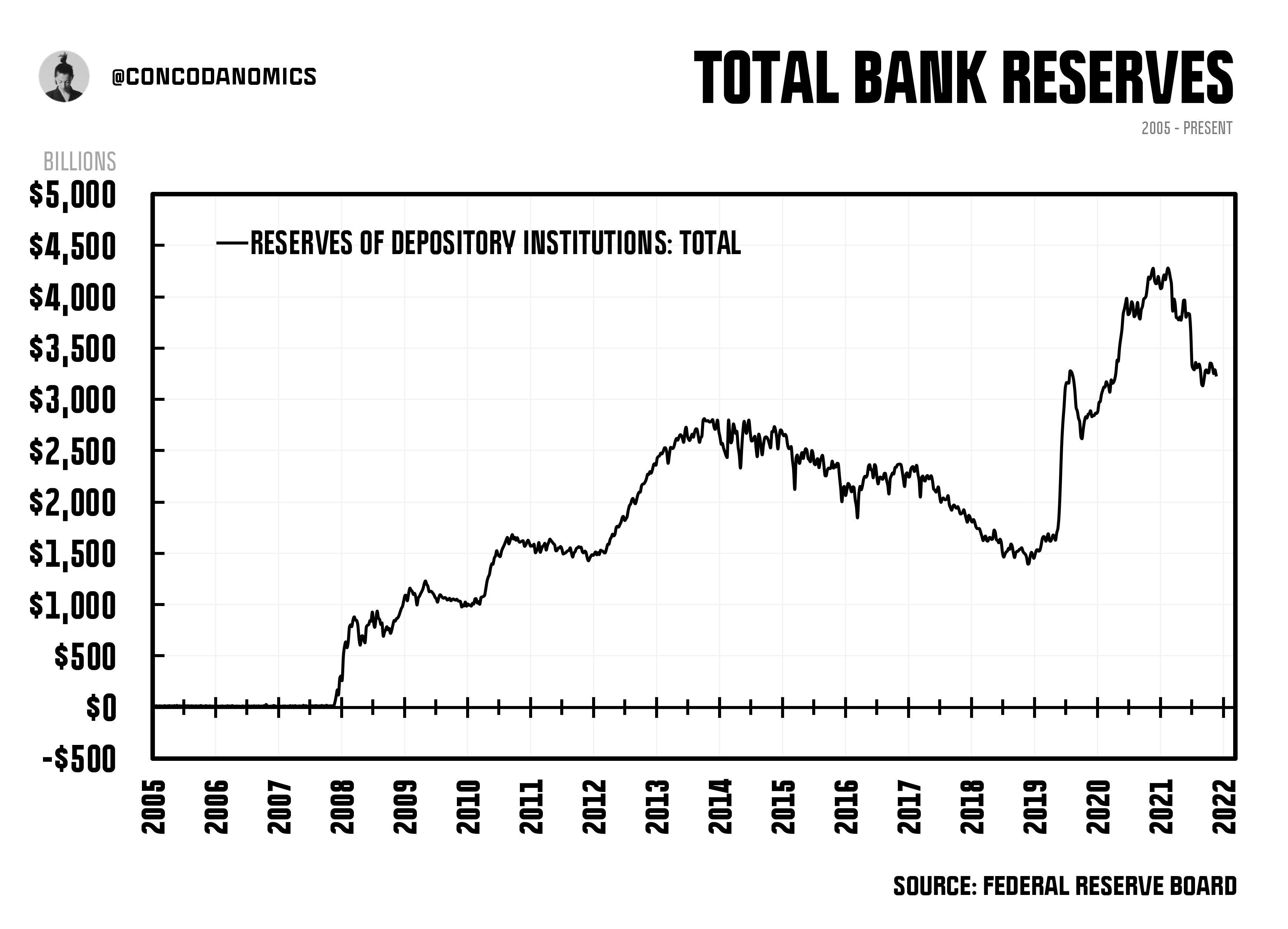

Then, in 2008, the Great Financial Crisis (GFC) hit, changing the central banking paradigm and the Federal Reserve System forever. The primary catalyst that fueled a radical transformation was the Fed officials’ decision to flood the system with bucketloads of reserves. The amount was staggering. In 2007, the system held a total of $15 billion in reserves. Today, that total has skyrocketed to roughly $3.2 trillion. The Fed’s latest quantitative tightening agenda has been aggressively eliminating bank reserves from the system. Still, it’s long before we return to “normal” levels.

With a system full to the brim with reserves, the Fed could no longer control interest rates through its previous policy of increasing and decreasing levels of interbank money. As shown in the graphic below, the Fed flooding the system with reserves meant that even sizeable supply adjustments no longer influenced the demand curve. The U.S central bank needed a new mechanism to take back control of Federal Funds and fast.

Enter the Fed’s “Ample Reserves” regime, where Fed officials stopped using open market operations (OMOs) — buying and selling government securities to alter reserve levels — as its primary tool to adjust the price of money. On October 6th, 2008, the Fed began paying reserve account holders, mostly large commercial banks and government-sponsored enterprises (GSEs), interest on their balances. IOER (Interest On Excess Reserves), as it was called back then, had been chosen as the Fed’s chief tool to control interest rates.

By offering banks IOER, a “risk-free” investment option, the Fed gained the power to control money markets through two mechanisms. First, through the “reservation rate,” the lowest rate that banks were willing to loan out funds to the market. Because the Fed started handing out a risk-free investment that paid superior interest (IOER), no entity would want to lend to others at rates lower than the Fed. This set a ceiling on how high rates could go, alongside the Fed’s second mechanism: arbitrage. Fed Funds rarely dropped beneath IOER because entities could create a risk-free arbitrage, borrowing Fed Funds at say 1% and depositing it at the Fed, which paid out 1.5%. The 50 basis points gap would eventually narrow to near zero, as Fed Funds participants competed to arbitrage the spread away.

With these two new levers, the Fed believed it had successfully regained control of money markets. If it wanted to alter rates, the Fed simply adjusted the discount rate and IOER at the same time and by the same level. If the FOMC (Federal Open Market Committee) was indicating that rates should rise, money markets could adjust, preemptively pricing in a tightening cycle.

From there, the Fed established a ceiling on interest rates, but a slight problem remained. They also needed to establish a floor on rates. Influential participants in the Fed Funds market, such as Federal Home Loan Banks (FHLBs), were ineligible to earn interest on their reserve balances. This meant they sometimes pushed money market rates below the Fed’s targets. To counteract this, the Fed created the overnight reverse repo facility, ON RRP. This offered a risk-free investment at a set rate to parties ineligible for IOER, thereby correcting the bug and setting a lower bound on interest rates. Money markets obeyed with minimal fuss.

For now, that was that. After implementing a trio of policy rates (IORB, ON RRP, and the discount rate), the Fed once again felt it had total control of money markets. Yet, it still held one weakness: repo, the shadow banking market that allowed parties to temporarily transform their Treasuries into quasi-bank deposits. By 2019, barely any entities other than a few government-sponsored enterprises (GSEs) still participated in the Federal Funds market, as most institutions now had all the reserves they needed. Instead, animal spirits and regulation pushed market participants into repo.

On September 17th, 2019, rates in the repo market exploded higher. Everyone wanted cash, but there was a shortage. Corporate tax payments and increases in Treasury issuance prompted a large decline in reserves. As a result, banks had to cut back on repo lending. Nobody could provide.

Responding to this demand-supply mismatch, the Fed created what it eventually called the “Standing Repo Facility”. This allowed specific entities to obtain cash from the Fed at a set rate using U.S. Treasuries, agency debt, or agency mortgage-backed securities as collateral. The Fed’s gambit worked. Since everyone started borrowing from the central bank, the Secured Overnight Financing Rate (SOFR), which tracks the cost of transactions in the repo market, fell from over 5% to within the Fed’s target range.

Fast forward to July 2021, after COVID and the ensuing QE Infinity, IOER along with IORR (interest on required reserves) had grown redundant. The Fed retired these measures in favor of a single benchmark: IORB (Interest on Reserve Balances). QE Infinity had made the term “excess reserves” meaningless.

Since then, it’s been plain sailing for the Fed. It has, at least for now, eliminated potential crises in money markets. If rates soar above its target range, the Fed adjusts IORB or fires up the Standing Repo Facility, bringing rates back into its desired range. At the lower bound, entities barely want to borrow under the Fed’s ON RRP rate, as they’re missing out on a risk-free investment from an entity that can issue debt with no credit or default risk. The Fed’s rate floor has been “leaky” a few times, but everytime it’s been fixed.

So by implementing a trio of policy rates (IORB, ON RRP, and the discount rate), and utilizing its Standing Repo Facility, the Fed has gained a solid grip on money markets. Ever since the repo market blowup, minus a few “hurdles”, the status quo has evolved into stability.

Now, claiming the system is “stable” is what many will deem contrarian. But contrary to popular belief, the Fed has created a more durable system and increased resilience. Most Fed analysis is ideologically driven, not based on validities, so it’s hard to acknowledge.

This, however, does not mean financial markets have been stripped of hazards. With the Fed being able to prevent domestic money market crises, the danger now lies offshore in exotic areas of the financial system.

But once again, the U.S is gradually gaining authority and power over these markets. By providing central bank swap lines and foreign exchange swaps to its closest allies, opening a FIMA facility to seemingly supply emergency dollars to China, and issuing $1 trillion in Treasuries every year till at least 2055, America will increase its grip on global finance, with the U.S. Dollar front and center.

It’s for these and many other reasons that Concoda sees the endgame as not a collapse but the Fed gobbling up every shadow banking paradigm to maintain financial stability. The REM Industrial Complex (Repo, Eurodollar, and Money Market Fund) will continue to fall under the Fed’s umbrella. The U.S dollar hegemony requires a complex, ever-changing financial system, and as it becomes increasingly elaborate and intricate, the Federal Reserve must expand its powers to preserve authority. The so-called world’s central bank possesses almost total control over most of the global monetary system, but if another threat emerges, it can — and will — adapt to the situation, changing the rules of the game once again to keep the monetary system functional and stable.

Despite a brief backlash, everyone — central bank critics, average citizens, and even crypto advocates — will go along with the Fed’s contemporary policies because the alternative is a financial catastrophe so ominous that even collapsitarians will choose to avoid it. When everyone is faced with the real consequences of the so-called Great Financial Reset™, it will be exposed as a mere daydream.

If you enjoyed this, feel free to smash that like button and share a link via social media. Thanks for supporting macro journalism!

with leaders now eager to prevent rising instability in America’s bond market. Their solutions, however, will not only prevent a calamity but stimulate risk assets without the aid of central banks. The era of “Treasury QE” awaits us.

After we warned late last year about rising illiquidity in America’s sovereign bond market, leaders have begun to respond. The unintended consequences of previous policies, regulations, and interventions can no longer be ignored. Earlier this month, authorities revealed their latest mechanism to paint over the cracks in the U.S. empire’s liquidity goliath. Officials announced the first Treasury buyback program in just over two decades, designed to thwart illiquidity in America’s $23 trillion sovereign debt market.

the entire U.S. Treasury market visualized

Over the last decade, the post-financial crisis regulatory establishment has forced the biggest liquidity providers in the Treasury market to retreat. The major players have pulled back from market-making, just as America embarks on its greatest debt expansion in recent history. Regulations such as Basel III and the Dodd-Frank Act have hindered the major liquidity giants through balance sheet constraints, such as the Supplementary Leverage Ratio (SLR) and Liquidity Coverage Ratio (LCR). The cost of making markets in Treasuries is ever-increasing.

Source: U.S. Treasury

Meanwhile, to achieve its global and domestic aims, the U.S. empire is set to issue around $1 to $2 trillion of (net) Treasury debt each year, all while the ability of financial actors to absorb such an amount is dwindling. Monetary leaders, however, have acknowledged the endgame. The rules and restrictions they have enforced over the last decade have been designed to transfer systemic risk from the big banks to the sovereign (state) level. But to also keep the global liquidity machine churning, they will need to conjure up more monetary alchemy.

Although the details aren’t yet set in stone, the U.S. Treasury will be conducting a Treasury buyback program in 2024 and onwards. It has two objectives: to improve “cash management” — jargon for reducing the volatility of the Treasury’s bank balance (the TGA) — and to boost liquidity in the secondary Treasury market.

Buybacks will also enable the Treasury to replace expensive bonds with those that cost less to service. What’s more, much like the Federal Reserve, the Treasury will become a “dealer of last resort”, acting as a buyer of illiquid bonds when no other participant is willing. Using funds from either bond sales or its bank account at the Fed, the U.S. Treasury will purchase existing bonds in the secondary market (via primary dealers such as JPMorgan and Nomura) to boost liquidity and maybe even suppress yields. Lower yields equal cheaper expenses.

Though Treasury buybacks give them the ability to greatly influence markets, officials have stated that the announced program won’t be extensive enough to act as a bailout in times of stress. If turmoil erupts, other measures will be enacted.

Today, though, the number of tools officials can employ to quash volatility has grown more limited than ever before. The Fed can’t initiate a full-blown pivot of rate cuts and QE without reigniting animal spirits, undoing all efforts to tackle inflation. Its toolbox remains scarce. Instead, officials at both the Fed and U.S. Treasury are doing everything in their power to continue a tightening cycle without reversing course. With a pivot off the table, they have been forced to implement what Concoda calls the “Not-QE corridor”, the new unconventional toolbox.

Much like the Fed’s “Global Jaws”, which depicts the global dollar rates corridor, the “Not-QE corridor” has an upper and lower limit. When the upper boundary is reached, financial conditions have become too loose for the Fed to sit by idly. More rate hikes and QT will follow. Conversely, when the lower limit is reached, financial conditions have tightened enough to warrant Fed intervention. The U.S. central bank has no intention of pivoting until it’s reached its 2% inflation target, so it must invent “stealth QE” facilities, like the BTFP (Bank Term Funding Program).

The Fed has been using all the easing and tightening tools available in its armory, but the U.S. Treasury has yet to wield any. At the upper limit of the Not-QE corridor, the Treasury has chosen to avoid deploying “TQT”: Tighter Quantitative Tightening. With TQT, monetary leaders attempt to tighten conditions further by reducing the Fed’s balance sheet at a faster pace while issuing more long-dated bonds to the market. The greater duration risk of longer-dated bonds causes investors to sell riskier assets to fund these purchases.

Meanwhile, at the lower limit of the Not-QE corridor, the Treasury does not possess any concrete tools to stimulate asset prices. After all, that’s the job of the Federal Reserve. At the start of 2024, however, buybacks will commence, enabling the prospect of Treasury QE.

If inflation remains higher for longer, and the Fed breaks something else not worth pivoting over, the Treasury could join forces with the U.S. central bank to help ease financial conditions. While the Fed implements more Not-QE measures, the Treasury uses buybacks to stimulate risk sentiment. Previous buyback programs have not been used by Treasury officials to specifically stimulate asset prices, yet this time could be different. If politics at the Treasury and the Fed align during a period where a pivot is undesirable, the Fed’s independence could be bypassed.

The first of two mechanisms they could use to stimulate financial assets via buybacks is simple: remove duration risk from the market by buying back longer-dated bonds and swapping them with shorter maturities. Swapping 30-year bonds for 2-year notes will be stimulative. Still, to truly make this “quantitative easing for Treasuries”, officials would have to announce that this is what they’re doing in advance, thereby mimicking the psychological effects that traditional QE (buying bonds with newly printed bank reserves) has on risk assets. Right now, the Treasury has no plans to employ this type of easing. Proposed buybacks will be “duration neutral”. But it’s feasible if desired.

Then, there’s the second Treasury QE mechanism, which this time boosts liquidity in the financial system and potentially increases risk-seeking behavior: Treasury buybacks where the newly issued bond is funded with cash drained from the Fed’s RRP (reverse repo) facility. Unlike the first kind of Treasury QE, easing occurs without Treasury officials ever intending to loosen financial conditions. If a money market fund (MMF) withdraws cash from the RRP facility, a Treasury buyback is all that’s needed to boost “net liquidity”.

Treasury QE visualized (click to enlarge)

Before this type of Treasury QE takes place, the MMF had originally invested in RRPs (reverse repo agreements) offered by the Fed. The result was a stable stream of overnight income for the MMF but a net draining of liquidity from the financial system. RRPs are what Concoda calls “reserve neutralizers”. Bank reserves and deposits are “neutralized” .i.e temporarily removed from the banking system and replaced with the most illiquid cash-like investment: an RRP issued by the Fed. Unlike other short-term investments, cash is locked in the triparty repo platform — which the Fed uses to process RRP transactions — till 3:30 pm the following evening. The price to pay for receiving free money from the Fed is “trapped” intraday liquidity and often inferior returns.

When the MMF invests in an RRP, its commercial bank destroys the MMF’s deposit and sends reserves to the Fed. Once received, the U.S. central bank transforms these reserves into an RRP liability on its balance sheet. Liquidity, in the form of bank deposits and reserves, has been “neutralized”.

The Fed’s RRPs remove bank deposits and reserves temporarily

But when the money fund decides to partake in a buyback by purchasing new bills the U.S. government is offering, this process “de-neutralizes” reserves and deposits, adding once-trapped RRP cash back into the banking system. Overall liquidity has expanded once again. This type of Treasury QE, however, can only be influential if MMFs are willing to unwind their RRP positions with the Fed and take part in upcoming buybacks. If investments other than RRPs, like bills and repo, offer superior returns, only then will this be stimulative. Ultimately, in both scenarios of Treasury QE, Treasury buybacks could be used as a QE-style signaling tool to further encourage investors to withdraw from money market funds (MMFs) and invest in riskier assets, thereby forcing more liquidity into the banking system.

Upon implementing Treasury QE, monetary leaders will have fitted the missing piece in their Not-QE corridor:

Treasury QE via buybacks and “Not-QE” from the Fed will provide a stronger lower bound to ease financial conditions when needed, while QT and TQT achieve the opposite effect. Moreover, if the Fed and Treasury have joint political goals, they can effectively bypass the Fed’s so-called independence, coordinating the easing and tightening of financial conditions. On the flip side, they could also offset one another’s actions. For instance, the Treasury could be “tightening” while the Fed “eases”.

For now, monetary leaders only need to activate some elements of the Not-QE corridor. U.S. Treasury officials have decided not to fire up TQT (Tighter Quantitative Tightening), while “Treasury QE” through buybacks could only come online after 2024 commences. QT (quantitative tightening) and “Not-QE”, meanwhile, remain active. QT is still shrinking the Fed’s balance sheet by $95 billion per month, whereas “Not-QE” is delivering a somewhat stimulative effect to risk assets, without the Fed ever printing reserves to buy bonds outright (actual QE).

Nobody, not even the Fed, seems to know what catalyst will cause officials to finally return to rate cuts, QE, or both. If inflation remains stickier for longer than most expect, the Not-QE corridor won’t collapse anytime soon, and monetary alchemy will prosper. The Treasury market provides those who oversee it the power to control global finance like never before. Yet they’ve chosen not to use it to its full effect. But with Treasury QE on the way, those in charge may give in to temptation. Eventually, these powers may be activated. It’s widely believed that officials are running out of ideas and tools to preserve stability. Yet in reality, the golden age of intervention is yet to come. When Treasury QE arrives, the Great Sovereign Debt Intervention™ will have only just begun.

If you enjoyed this, feel free to hit the ♡ button to let us know and share a link via social media to help us grow. Comments are also encouraged. Thanks for supporting macro journalism!

Thanks for reading. If you enjoyed this, you can support our work by buying us a coffee and becoming a subscriber. You’ll receive access to all the content we put out, gain access to discussions, direct email, and more.

If you act on anything provided in this newsletter, you agree to the terms in this disclaimer. Everything in this newsletter is for educational and entertainment purposes only and NOT investment advice. Nothing in this newsletter is an offer to sell or to buy any security. The author is not responsible for any financial loss you may incur by acting on any information provided in this newsletter. Before making any investment decisions, talk to a financial advisor.